Temporary Regulations for “Early Elect In??

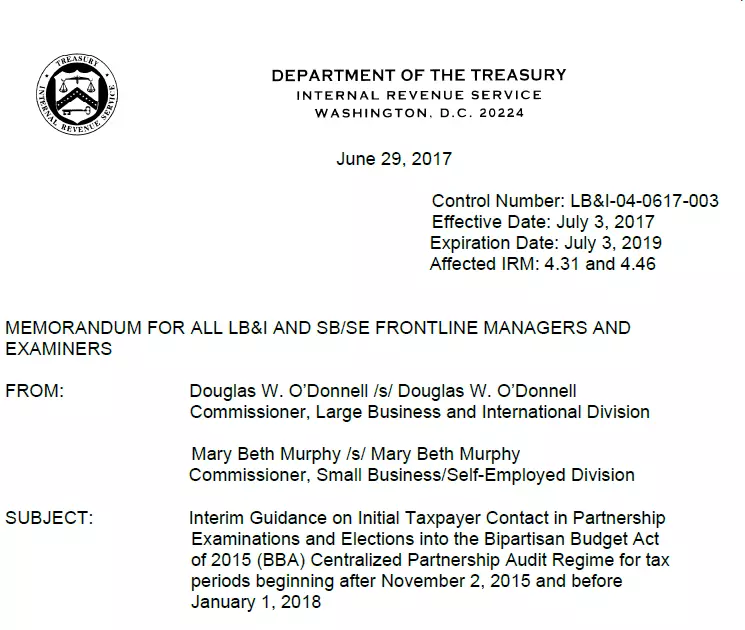

The Treasury Department released a memo on June 29, 2017 from the LB&I (Large Business and International Division) and SB/SE (Small Business/Self-Employed Division) providing interim guidance for examiners on how to handle “early elect in?? partnerships who filed returns after November 2, 2015 and before the January 1, 2018.

The memo addresses the temporary regulations (§301.9100-22T) for the “early elect in?? and explains the process of an election which must be made within 30 days of the partnership receiving written notice that their return has been selected for examination.

A New Era of Partnership Representation Before the IRS

Search

Recent Blog Posts

- Surge in BBA Partnership Audits Expected in 2022

- IRS Releases Memo Concerning Access to Administrative File in TEFRA and BBA Examinations

- IRS Provides Penalty Relief for New Capital Reporting Requirements

- IRS Releases Proposed Regulations on Centralized Partnership Audit Regime

- Centralized Partnership Audit Regime Website Launched by IRS

- Partnership Filing Relief

- IRS Issues LB&I Memorandum

- IRS Release Clarifications for Form 8082

- IRS Release Draft Instructions to Form 8978

- IRS Releases Interim Guidance Centralized Partnership Audit Regime

Bios

Archives

- January 2022

- April 2021

- January 2021

- November 2020

- September 2020

- April 2020

- March 2020

- February 2020

- November 2019

- October 2019

- July 2019

- March 2019

- January 2019

- December 2018

- November 2018

- September 2018

- January 2018

- October 2017

- August 2017

- July 2017

- May 2017

- February 2017

- January 2017

- November 2016

- October 2016

- September 2016

- August 2016